Per reporting by Bloomberg Law, US multinational corporations are tactically restructuring their overseas holdings to potentially delay the impact of the newly established 15% global minimum tax. This strategic reorganization, which involves dissolving holding companies and moving the ownership of foreign subsidiaries back to the US, could defer tax obligations under the global minimum tax framework, possibly indefinitely.

Tax professionals have been assisting US companies with these "out-from-under restructurings," though the identities of the companies remain undisclosed. The restructuring activities may become more visible in corporate annual reports at the end of the fiscal year. Chad Hungerford, a partner at Deloitte Tax LLP, confirmed the occurrence of these shifts among his clients.

The US, which has not yet committed to the global minimum tax, presents a unique position for its multinational companies. The restructuring is seen as a bet on a one-year delay becoming permanent, contingent on the outcome of the upcoming November election and the potential reluctance of other countries to enforce tax collection from US businesses.

However, the global tax agreement includes an "undertaxed profits rule" (UTPR), set to take effect in 2025, which allows compliant countries to tax multinational companies if their parent and local jurisdictions do not apply a 15% rate. This rule presents a dilemma for these countries: whether to tax US foreign subsidiaries, risking retaliatory action, or to permit avoidance of the global minimum tax, undermining the OECD-negotiated tax deal.

Steffie Klein, a senior associate and tax adviser at Loyens & Loeff in Amsterdam, highlighted the importance of belief in the UTPR's effectiveness. Without it, companies could save on taxes until the US adopts the global minimum tax's second pillar.

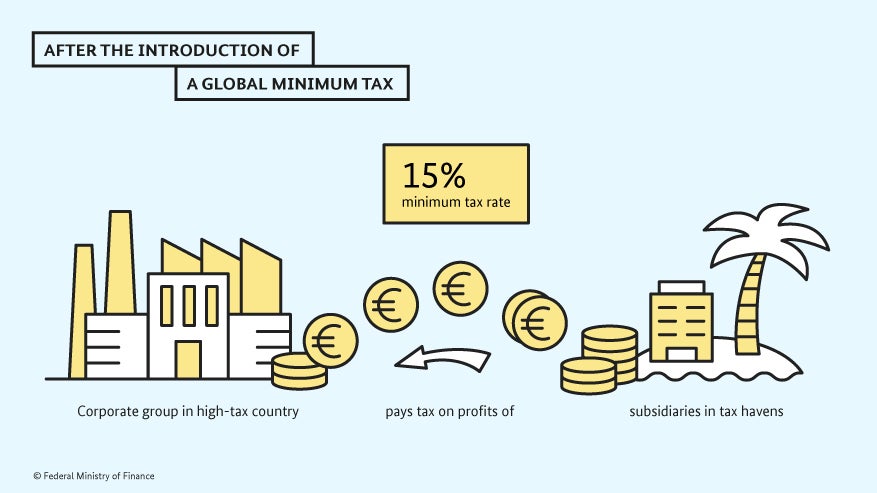

The global minimum tax aims to harmonize tax rates and reduce incentives for profit shifting. Thirty-six jurisdictions have implemented or plan to implement the tax as part of a 2021 international tax deal. The tax's effectiveness depends on three mechanisms: a qualified domestic minimum top-up tax, the income inclusion rule, and the UTPR.

Michael Lebovitz, an international tax partner at Eversheds Sutherland, noted that clients with holding companies in Switzerland and the Netherlands are among those reshoring subsidiary ownership to the US.

Despite the costs, the restructuring strategy may be financially advantageous for companies expecting higher tax payments and significant compliance costs under the new tax regime. Corporations such as Johnson & Johnson, Eli Lilly & Co., and Zimmer Biomet Holdings Inc. have forecasted tax rate increases, while Carnival Corp. anticipates up to $200 million in additional costs annually.

The compliance burden is also a driving factor, as companies must ensure adherence to the law across various business segments. Pfizer Inc.'s CFO Dave Denton mentioned the substantial increase in required disclosures for multinational companies.

With subsidiaries causing complexities in tax calculations, US multinationals are evaluating whether restructuring would be less costly than the added compliance expenses and potential rate increases. Tax practitioners report widespread discussions about mitigating exposure to the global minimum tax.

The strategy's effectiveness is time-bound, as the UTPR looms in the near future. It remains to be seen whether countries that have adopted the UTPR, such as EU members, the UK, and Korea, will enforce it against US subsidiaries, potentially provoking reactions from the US government.

With the global tax landscape in flux, the actions of US firms and the responses of international counterparts will shape the future of corporate taxation and international economic relations.